Finance

21.1 Our terms of reference require us to consider “the best use and management of the financial and manpower resources of the National Health Service”. In practice these resources are linked and about three quarters of the expenditure of the NHS goes on salaries and wages. It is important to remember that discussions of NHS finance must take account of its implications for NHS workers who account for about 1 in 20 of the total working population of the UK.

21.2 In this chapter we consider what should be spent on the NHS, how it should be raised, its distribution and its management. To help our work we commissioned studies on the management of financial resources and a critique of the health departments arrangements for allocating finance to health authorities These studies have provoked some public discussion and we hope have been useful to those working in the NHS. They have certainly been most useful to us.

What Should be Spent on the NHS?

21.3 Expenditure on the NHS in the financial year 1978/9 was about £8,100m, or over £140 for every person in the UK. Over 94% of this was revenue expenditure: only about £460m was spent on hospital building and other capital development. Since 1949 total expenditure on the NHS in real terms has more than doubled and the volume of resources devoted to the NHS has increased in every year except 1952. Total NHS expenditure has grown faster than the rest of the economy in almost every year since 1954, rising from 3.4% of the gross domestic product (GDP) in 1954 to 5.6% in 1977.

21.4 Nonetheless, many of those who gave evidence to us considered that expenditure on the NHS was nothing like enough. The BMA told us that:

“for some years now the money allocated by the Government for the service has been quite inadequate to meet the demands made upon it by the public”

and the TUC argued that:

“In the longer term an increased proportion of the national income must be devoted to the health service.”

21.5 Our evidence proposed amongst other things that more money should be spent on improving the hospital stock and services for children, the mentally ill and handicapped, and the elderly. There is no doubt that more could be spent, and spent well, on all of these. There were few suggestions for economies. The effect of lack of resources on morale in the NHS, and the low pay of some NHS workers were also mentioned. We had no difficulty in believing the proposition put to us by one medical witness that “we can easily spend the whole of the gross national product.”

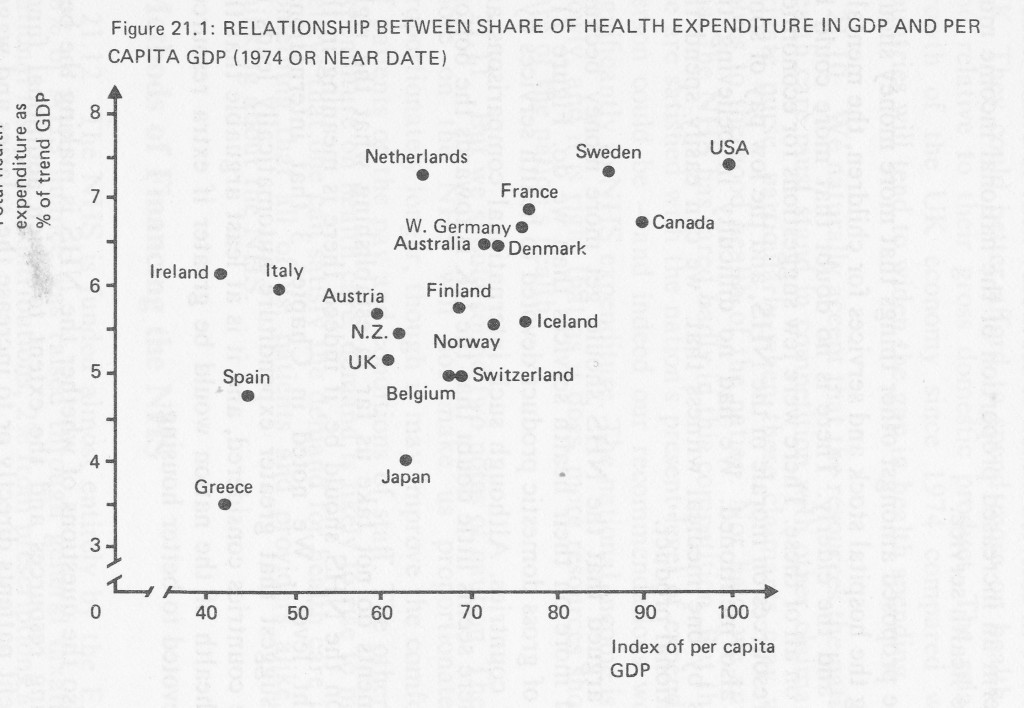

21.6 It was also argued that the NHS should get more money because other countries spend more on their health services than we do. Figure 21.1 shows the proportion of gross domestic product devoted to health services by a number of developed countries. Although such international comparisons are not wholly reliable there seems little doubt that the UK is towards the bottom of the league.

21.7 These arguments do not take us far in establishing what the right level of expenditure on the NHS should be, if indeed there is meaning in the concept of “the right level”. We noted in Chapter 3 that international comparisons do not suggest that greater expenditure automatically leads to better health in those countries considered, and it is at least arguable that the improvement in the health of the nation would be greater if extra resources were, for example, devoted to better housing.

21.8 There are also the questions of whether the NHS is making the best possible use of existing resources and the extent to which additional funds would be used to benefit patients directly or to increase the salaries and wages of NHS workers. We consider that NHS gives good value for money, but there is still considerable room for improvement. Regional Administrators in England told us:

“The National Health Service has become accustomed throughout the 25 years preceding reorganisation to the prospect of continual growth in the financial resources available to it. Though agreeable, the result has been to allow slack management, with no incentive to examine obsolete patterns of spending, or to develop a coherent plan for the future.”

This view was supported by other evidence that we received, by the research studies we commissioned and by much unofficial and official published material. The government’s priorities document, “The Way Forward” for example, contains an interesting appendix listing ways in which resources could be more efficiently used. It is essential that a service which spends three quarters of its budget on manpower should make efficient use of its labour force.

21.9 Figure 21.1 indicates that many of those countries which devoted a greater share of their resources to health services in 1974 were richer than the UK. They could better afford to spend more on health care both absolutely and relative to their gross domestic product. The relatively slower rate of growth of the UK economy since 1974 compared with many developed countries will tend to widen the gap in health spending.

21.10 We naturally accept that the resources the nation devotes directly to health care must stand in competition with other claimants on the public and private purse, particularly when those claimants may well contribute them selves to the good health of the nation. Nor have we any evidence to suggest that the NHS has fared badly in this competition. But this does not mean that we are satisfied with the nation’s present level of expenditure – no thoughtful person could be – and indeed our recommendations would, if adopted, add significantly to NHS expenditure. The national income is growing, if relatively slowly, and it is right that as it does, more resources should be devoted to the care of the nation’s health.

21.11 But we should sound two notes of caution. The first is that spending more on the NHS will not make us proportionately healthier or live proportionately longer, though it may improve the comfort and quality of life of patients or the pay and conditions of staff. The other is that whatever the expenditure on health care, demand is likely to rise to meet and exceed it. To believe that one can satisfy the demand for health care is illusory, and that is something that all of us, patients and providers alike, must accept in our thinking about the NHS.

Methods of Financing the NHS

21.12 The NHS is funded almost entirely by the Exchequer. In 1978/9, 88% of NHS finance was raised through general taxation, 9.5% from NHS national insurance contributions, 2% from prescriptions and other charges, and the balance from other sources such as sale of land and port health charges. The proportion of finance from general taxation has risen since the early 1960s, while the importance of both the NHS insurance contribution and revenue from charges has declined. At no stage has less than 94% of NHS expenditure been raised from general taxation and NHS insurance contributions.

21.13 We received several proposals for changing the arrangements for financing the NHS. Their purpose was either to supplement the Exchequer contributions, or to replace it with a system which might encourage more efficient use of resources or which might have greater public appeal. We discuss the main proposals below, but there is one general point to be made It must be understood that there is no escaping government supervision of health service expenditure whatever system of raising funds is adopted. Some advocates of an insurance system evidently see it as a mechanism for automatically increasing expenditure on the NHS as costs rise. They delude themselves if they do. The rising cost of health care is a major concern in most developed countries, and measures to control it may be, and are, introduced whatever the method of financing health services.

Insurance financing

21.14 We noted in Chapter 4 that in Western Europe and North America health care is commonly financed by insurance schemes. A number of those who sent us evidence thought that this should be the arrangement in the UK. We consider the advantages and disadvantages of insurance based schemes below, but it is important to understand that their existence elsewhere is not usually the result of some careful weighing of the advantages or disadvantages of different methods of financing health care. Health insurance schemes come in a great variety of shapes and sizes, they have in most cases grown up over many years, and they reflect the peculiarities of the countries they serve. The UK in unusual in that a deliberate decision was taken in 1946 to introduce an Exchequer financed national health service.

21.15 There is no standard system of health insurance, and when considering the theoretical virtues of such a system we made assumptions about what its main characteristics might be, based on the private health insurance schemes in the UK at present. There are perhaps four essential differences between the NHS and the kind of health insurance scheme that might be introduced:

- charges to patients – each patient would be charged accordingly to the service used and wholly or partly reimbursed by an insurance agency;

- insurance could be undertaken by private agencies on a commercial basis or by some form of public undertaking;

- all those covered by insurance would have some choice of the extent of the cover they purchased;

- the individual or his employer would pay for insurance cover.

People would buy health insurance much as they buy house or motor insurance. There would be competition between companies, and there might be a compulsory minimum level of health insurance in much the same way as owners of motor cars are obliged to take out third party cover. There would be good risks and bad risks among users, and premiums might vary accordingly.

21.16 We have assumed that the system would be voluntary, perhaps with compulsory elements, because arrangements under which everyone had to pay for the same cover for themselves and their families would not in practice be significantly different from those we have at present. Instead of paying for the health service through taxation, individuals would be compelled to do so through insurance institutions. Indeed, many foreign insurance based systems contain such a large compulsory element that they could be described as “tax financed”. The introduction of choice, and the competition that goes with it, would be essential if an insurance system were not to be indistinguishable from an Exchequer Financed system.

21.17 The introduction of an insurance system would not itself lead to more resources being devoted to the NHS, but there might be other advantages. It might be that patients, becoming more directly aware of what health care costs, would become more responsible in their demands on the However, fully insured patients would have little direct incentive to economic use of the service, because the extra costs imposed by their demands on it would be spread over the premiums of all those insured. By the same token, there would be little inducement for providers of the service to keep their costs down.

21.18 Some doctors and other health professionals favour a system of remuneration based on item of service payments. They argue that the detailed itemisation necessary would provide rapid and useful information which could be used for the monitoring of services, and that while health professionals are often paid more under such systems they work harder and more effectively so that labour costs are lower than under a salaried system. But insurance financing does not require that professionals should be paid on an item of service system, though it is often associated with it. Nor does item of service remuneration require insurance financing.

2.19 There are two important disadvantages which arise in most insurance based schemes. First, there are groups in the community who are both bad health risks and too poor to pay high premiums. They include elderly people, children, and the mentally and physically handicapped. Over 60% of NHS expenditure is currently accounted for by these groups, and nearly half of the community are exempted for one good reason or another from prescription charges, for example. We noted in Chapter 3 that poorer people tend to have worse health, but they are of course also least able to pay insurance and are most likely to be deterred by charges at time of use. The imbalance between ability to pay for health care and the need for it is met in most countries by government support. However, an insurance scheme which offered a range of benefits according to ability to pay would inevitably favour the wealthier members of society. It is true that there are inequalities now in the availability of health care: private medical care may be purchased, and, as we have seen in earlier chapters, there are geographical and social differences in access to health services under the NHS. But private medicine is provided outside the NHS, and the differences of availability of health services within it are recognised as faults to be eradicated so far as possible. The introduction of an insurance system would incorporate into the NHS a new principle, namely that a different standard of health care under the NHS was available to those who chose to pay for it. Some may feel such a change to be desirable, but at least it should be clearly recognised for what it is.

21.20 The second disadvantage is the cost of administration. The bulk of NHS funds are collected through general taxation. No special mechanism is required. An insurance system would require insurance companies to determine premiums, collect them and distribute them in the form of payment for services either to the claimant or to the hospital or practitioner who had provided the treatment. A mechanism for helping those too poor to pay premiums would be needed. It seems to us that this would inevitably lead to more forms to fill in and more people to handle them. An OECD study in 1977 indicated that the expense of collecting contributions and making payments to suppliers of medical services were probably higher in most countries than in the UK.

21.21 We do not think that the NHS should be funded by health insurance. The advantages of the market place could well be real but there would certainly be significant disadvantages. In addition the introduction of such a system in the UK would mean a great deal of upheaval – everyone would have to get used to making the new system work. The advantages of change would have to be much more clearly demonstrable than they are at present to make this worthwhile. No doubt there are grounds for criticising the equity and efficiency of the current system, but we do not think that an insurance based system is the best means of effecting improvements.

21.22 We have ruled out a complete change to insurance finance but what of less radical alternatives? It was suggested to us that the existing private insurance arrangements in the UK might be encouraged and extended in a variety of ways. For example, free use of the NHS might be restricted to those below certain income levels and the richer and healthier members of the community expected to finance their consumption of health care through private insurance. Insurance premiums could be made allowable against income tax. The effect might be to inject extra resources into health care with benefits to both NHS users and those who opted for the private sector.

21.23 Partial insurance financing implies expansion of the existing private health care sector. It would have many of the advantages and disadvantages of a system based primarily on insurance funding but would not involve the same major upheaval and its associated costs. However, there would be the danger of producing the two tier system of health care we have referred to. We would have serious reservations about actively encouraging a system in which the richer members of our society received better care than the less well off.

Supplementary finance

21.24 We have said that the government was likely to control NHS expenditure whatever the method used to finance it. Unless Parliament concludes that more money is indeed needed, a new scheme for raising substantial extra funds for the NHS is likely to be adopted only if it either represents a more politically acceptable approach than the equivalent Exchequer financing, or if it is seen as a means of changing the way that those who use and work in the NHS behave. Trivial additions to NHS resources might be disregarded by those who control NHS expenditure, but would not assist an under-financed service; while a substantial addition would probably lead to a reduction in funds made available from the Exchequer.

Charges

21.25 Charges to NHS patients yield about £l25m per year or about 1.6% of the cost of the NHS. About half of this arises from dental charges and about a quarter each from charges for prescriptions and ophthalmic services. As Table 2 shows, their revenue yield in recent years has fallen in proportion to the cost of the services. It was suggested to us that there should be both a considerable increase in existing charges and that new ones should be introduced. The new charges proposed included “hotel” charges for non-medical services in hospital, for visits to hospital accident and emergency departments, and for consultations with general practitioners.

21.26 Purely as an illustration we show in Tables 21.3 and 21.4 what might have been the effect in the 1975/6 financial year of increasing the prescriptions charge to 50p, and introducing a hotel charge for inpatients of £20 per week, an accident and emergency visit fee of £5, and GP consultation charge of £2. On these figures Table 21.3 shows that after adjustments for reductions in use of the service due to the charges and for increases in social security payments, public expenditure would have been cut by approximately £440m. This saving would have been reduced by the administrative costs of collecting revenue from new charges. An estimate of what would have been the revenue in 1975/6 from unchanged dental and ophthalmic service charges, a higher prescription charge and possible new hospital and GP consultation charges is given in Table 21.4. On the assumptions made, but without allowing for higher administrative costs, the total revenue from charges to NHS patients would have amounted to about £423m or 8.0% of NHS expenditure in 1975/6.

TABLE 21.1 Revenue from Principal NHS Charges: Great Britain 1972/3-1978/9

Financial years

| Service | Charge revenue, £m | Revenue as % of cost of service | ||||||||||||

| 1972/3 | 1973/4 | 1974/5 | 1975/6 | 1976/7 | 1977/8 | 1978/9 | 1972/3 | 1973/4 | 1974/5 | 1975/6 | 1976/7 | 1977/8 | 1978/9 | |

| General pharmaceutical | 27 | 28 | 28 | 27 | 28 | 28 | 29 | 9.9 | 9.4 | 7.8 | 5.8 | 4.8 | 3.9 | 3.4 |

| General dental | 30 | 33 | 34 | 37 | 45 | 58 | 63 | 23.4 | 23.2 | 19.4 | 16.0 | 17.7 | 22.5 | 19.1 |

| General ophthalmic | 16 | 17 | 19 | 20 | 26 | 27 | 31 | 51.6 | 50.0 | 45.2 | 27.8 | 34.2 | 35.2 | 34.4 |

Source: compiled from health departments’ statistics.

Note: Charges to private patients are excluded. Charges to NHS patients are also made for amenity beds, for certain items, such as wigs, dispensed in hospital out-patient departments and under the Road Traffic Act which permits the recovery through motor insurers of a contribution towards the hospital cost of treating road accident casualties.

TABLE 21.2 Estimated Effects of Illustrative New and Increased Charges: Great Britain 1975/6

£ million

| 50p prescription charge | £2 GP consultation fee | £5 accident and emergency department visit fee | £20 per week “hotel” charges for inpatients | Total | |

| Increase in revenue1 | 35 | 134 | 27 | 143 | 339 |

| Reduction in NHS costs2 | 14 | 13 | 6 | 84 | 117 |

| Reduction in NHS expenditure | 49 | 147 | 33 | 227 | 456 |

| Increase in social security payments3 | 16 | ||||

| Reduction in public expenditure | 440 |

Sources: health departments’ statistics;

Notes: ‘ It has been assumed that (a) 60% of prescriptions, g.p. consultations, visits to A and E departments and inpaticnt days would have been exempted from these charges; (b) the new charges would have caused a 10% reduction in the non-exempted g.p. consultations, A and E department visits and inpatient days: (c) the higher prescription charge would have reduced the number of non-exempt prescriptions by the 7.9% suggested by Lavers’ study.

2 The cost reductions have been estimated by taking the average NHS cost of a prescription, a g.p. consultation and a visit to an A and E department in 1975/6. The reduction in hospital inpatient costs arising from a hotel charge is based on the assumption that the charge reduces the length of stay in hospital, not the number of stays, so that the cost saved is that of days at the end of stays which is about half the average cost of all days in hospital.

” It is assumed that those inpatients who received reduced social security payments in 1975/6 while in hospital would have had their benefits increased to cover the hotel charge. If such patients had instead not had to bear the charge the increase in NHS revenue would have been reduced by £16 m.

No allowance has been made for the additional administrative costs of the new charges.

TABLE 21.3

Estimated Yield of Illustrative New and Increased Charges to NHS Patients1: Great Britain 1975/6

| Charges | Revenue | |

| £m | % of | |

| (1975/6 prices) | service cost | |

| New charges: Hospital (£5 accident and emergency visit fee, £20 weekly ‘hotel’ charge) | 170 | 4.2 |

| GP consultation fee (£2) | 134 | 41.9 |

| Higher prescription charge (50p) | 62 | 13.7 |

| Unchanged charges: Dental | 37 | 16.0 |

| Ophthalmic | 20 | 27.8 |

| TOTAL: | 423 | 8.0 |

Source: compiled from health departments’ statistics.

Notes: Excludes charges to private patients and hospital outpatients, amenity bed and Road Traffic Act charges.

The effect of the possible new and increased charges on use, and hence the cost, of the services has been allowed for in calculation of the proportion of the cost of the services recovered in charges.

No allowance has been made for the additional administration costs of the possible new charges.

21.27 Though a small proportion of total NHS expenditure, this is too large a sum to be ignored when the Exchequer contribution to the NHS is calculated. The only reasons for introducing the charges referred to would therefore be to discourage patients from using the services in question or to transfer part of the financial burden of the service from the taxpayer to the patient. But the patient does not become a major user of NHS resources until he becomes a hospital patient, and he becomes a particularly large user if he is admitted as an in-patient. In general, to be admitted as an in-patient requires not only the willingness of the patient himself but also the clinical judgement of at least two doctors. It follows that there can be little abuse of hospital resources by patients, and that if incentives and disincentives are to have a major effect on the use of hospital resources then they must be offered to doctors and not to patients. This does not apply to visits to GPs, but would the extra administrative costs and inconveniences of charges be compensated for by keeping away from GPs those who demand his service frivolously? We doubt it, and we would be uneasy that it could well discourage patients from seeking help when they really needed it.

21.28 We have put forward only the practical arguments against NHS charges though we acknowledge that there is a sizeable body of opinion that sees them as wrong in principle. But it will be apparent that we are not enthusiastic about charges. Indeed, we feel that, particularly with the irrational structure of charges we now have, there is a good case for their gradual but complete extinction, and we so recommend. The cost to the taxpayer of complete abolition might be about £200m of which £80m would represent the costs of meeting the resulting increase in demand.

21.29 We should not want to be misunderstood on this important issue. The way the public pays for the NHS is a matter which lies within our terms of reference only insofar as it affects the way the NHS uses its revenue or the way the public uses the NHS. The external issues of how tax or charges affect the public and public policy are certainly not our concern and must lie in the hands of the government. If we could see that the charges, which exist now made for better doctoring or discouraged frivolous use of the NHS by the public, then we should applaud them. But we do not see them in that light.

Other sources of finance

21.30 Other suggestions for supplementing sources of finance included a state lottery and some form of local voluntary funding. The main drawbacks to relying on a lottery to fund a significant part of the cost of the NHS, are its unreliability and the expense of collecting funds in this way. It should also be remembered that the yield from a national lottery would, in comparison with the £8,100m spent on the NHS at present, be very small. The Royal Commission on Gambling advocated a “National Lottery for Good Causes”. They calculated that this would yield in the first year about £37.5 million. Even if the whole of this were spent on the NHS it would still amount to under 0.4% of its cost. While we would certainly not wish to suggest that such an additional sum be rejected if it were offered to the NHS, its effect, though important at the local operational level, would be at very best marginal in a national context. The experiences of local authorities with fund raising from lotteries has not always been very encouraging.

21.31 We were told that the public would, with suitable encouragement, be prepared to make a significant extra financial contribution to the NHS. There is already much public involvement in the NHS through organisations such as Hospital Friends and the various societies for helping particular groups of patient. At one remove from the NHS, there are fund raising and research organisations like Age Concern, MIND and the Imperial Cancer Research Fund, which give valuable help but have a national rather than local impact. Local fund raising by voluntary workers is normally directed to a specific purpose, and can be a most welcome contribution. On the other hand, the more glamorous causes – new buildings or expensive equipment – are not always those for which the need is greatest, and may themselves commit NHS funds which are urgently needed for other purposes. We would like to see a continuation and expansion of the present voluntary effort, but we do not see it contributing significantly to NHS funds.

21.32 We can see advantages in local authorities being able to contribute to NHS funds if they so wish. There may be circumstances in which it would be in the rate payers’ interests to do so, and a local authority contribution to the NHS – the reverse of the present joint financing – would be a tangible expression of local government’s involvement, as well as giving its representatives more influence on the health authority.

Hypothecation

21.33 Some of our witnesses favoured greater hypothecation of tax revenue to cover NHS expenditure, i.e. setting aside from general tax revenue some or all of the proceeds of a particular tax or taxes to be spent exclusively on the health service. The arguments for this suggestion varied depending on the precise arrangements proposed, but two common themes were, first that the health service should have a source of revenue outside the control of politicians and insulated from the fluctuations in government economic policy; and, second, that hypothecation would increase the funds available to the NHS. It was also suggested that hypothecated taxes on health harming goods such as tobacco and alcohol would both appropriately penalise their users, and reduce their consumption and therefore the need for health service expenditure. Others felt that a hypothecated “health tax” levied directly on individuals on the lines of the NHS National Insurance contribution would be a useful reminder of the cost of health services.

21.34 We have noted above that no government is likely to relinquish control over NHS expenditure however it is financed. Hypothecation by itself would therefore neither increase spending on the health service nor remove it from political control. There are also objections to the particular arguments for a health tax or hypothecated taxes on health harming goods. A health tax levied at a flat rate would bear most heavily on the poorest tax payers; but if such a tax varied with income it would not provide the same signal to all individuals about the cost of the NHS. In any case since payment of a health tax would be unrelated to demands on the service made by the individual it would provide little incentive to its more economical use. Increasing the price of health harming goods by taxation might make consumers more aware of their dangers, but this could be achieved whatever the revenue of such taxes was spent on.

Distribution of Resources

21.35 In the discussion of the objectives of the NHS in Chapter 2 we stated our belief that the NHS ought to aim to provide equal access to health services for those equally in need irrespective of where they lived. We concluded in Chapter 3 that while there had been some improvement since 1948 in meeting this objective much remained to be done. We commissioned a critique of the health departments’ arrangements for allocating financial resources in the NHS from Martin Buxton and Rudolf Klein (referred to in paragraph 21.2 above), published in August 1978. We limit ourselves here to describing briefly some of the main issues. As usual, the problems in England seem to be greater than those in the other parts of the UK, and for that reason our discussion concentrates on England.

21.36 The big spenders in the NHS are hospitals and they account for over 70% of all NHS spending. In 1950/51 the best provided regional hospital board had received more than twice the allocation per head of the worst By 1971/72 the best provided RHB received only about one-third per head more than the region with the lowest allocation. There had been no systematic attempt to assess overall need, though various mechanisms, including in particular the 1962 Hospital Plan, had attempted to direct resources to where they seemed to be most required.

21.37 In 1970, in an attempt to reduce geographical inequality further, the DHSS introduced the “Crossman” formula as the basis for distributing funds to RHBs. Under it, half the money allocated was based on the population served, and a quarter each on the number of beds and the number of cases

21.38 The Crossman formula was succeeded by the arrangements recommended by the Resource Allocation Working Party (RAWP) which reported in September RAWP recommended that revenue funds should be allocated according to relative need for health care, and that no account should be taken of previous allocations. The formula used population, adjusted for age and sex and marital status as well as standardised fertility ratios and standardised mortality rates as the basic measures of need. Adjustments were made for cross-boundary flows of patients and the high cost of providing

services in London. Separate allowance was made for teaching activities through the service increment for teaching (SIFT). The Working Party recommended that its principles should be applied within regions, and that a population based formula should be used for calculating capital funding.

21.39 In Scotland, Wales and Northern Ireland similar exercises took place and broadly similar recommendations were made. Teaching hospital costs were more fully protected than in England, and there were other differences related to the size and particular needs of those parts of the UK.

21.40 The introduction of the RAWP formula was an important step towards determining a rational and equitable system of allocating resources to health authorities. It represents a clear commitment to reduce inequalities in health care provision, which have existed since 1948. The ingredients of the formula itself are partly a matter of subjective judgement and political decision, and we consider it essential that they should be open to public inspection and debate. The publication of the RAWP report provides for this. We hope that developments of the formula will similarly be laid open to public inspection

21.41 While the RAWP approach is sound in principle, it has been subject to a good deal of criticism. The use of mortality rates as measure of morbidity, the valuation of the capital stock and the failure to include, or allow for, family practitioner services have aroused much concern. Nor does the formula take account of factors which may be important locally in determining the need for resources, such as the occupational status of the population, social deprivation and the availability of other public services. Its application within regions has been widely criticised. It is clear that judgement must be used to temper any rigid application of the formula below the regional level. These and other issues are discussed in the commentary prepared for us by Buxton and Klein referred to above and we do not propose to go into them in detail We understand that the DHSS have established an advisory group on resource allocation to consider how the formula may best be modified. A formula is only as good as the data on which it is based, and if this is unsatisfactory confidence in it will be undermined. The RAWP report listed a number of aspects of their study on which research was required, and we do not doubt that the DHSS and the other health departments will encourage this.

21.42 We discussed in Chapter 17 the particular problems faced by the teaching hospitals, especially in London, as a result of the introduction of the RAWP formula. While a part of the additional cost of teaching hospitals is covered by the SIFT element of the RAWP formula, this still leaves a substantial part of the additional cost to be met from the normal RAWP In particular the additional costs arising from research activity and from the role of the teaching hospitals as “centres of excellence” are not explicitly recognised. RAWP recommended that research should be set in hand on these matters, and we endorse the recommendation.

21.43 RAWP and the equivalent exercises outside England relate only to distribution of NHS funds within these parts of the UK. There is no explicit formula for the distribution of funds to the four parts of the UK, though there are marked differences in the resources provided, as the Buxton and Klein study shows. There may be adequate justification for these differences, but if so it should be explained and made public in the context of an explicit formula for the distribution of funds to the health service in the four parts of the UK. We recommend accordingly.

Financial Management

21.44 We asked Professor Perrin and his team to investigate the financial management of the NHS. The report which they produced concluded that NHS funds were being ‘”properly spent’ in the sense of the technical probity of the spending, and on purposes broadly consistent with [health] departmental policy”. However, they identified a number of weaknesses, some of them serious, in the system of financial management of the NHS. The financial control systems were “little used for planning and decision-making in any positive sense of resource allocation or conscious testing of alternatives” and the system of financial management was not conducive to the efficient and economical use of the service’s resources. We commend the report to the health departments and health authorities. We examine briefly below some issues to which we would like to draw particular attention or which were outside the scope of the Perrin study.

Equipment and supplies

21.45 The NHS spends over £900 million a year on a wide variety of equipment and supplies. These include food, fuel, bed-linen, surgical dressings, surgical equipment and drugs as well as major items of scientific and medical equipment. The suppliers of the NHS range from very large multi-national companies to small local firms. The regional supplies officers described the supplies organisation of the NHS in evidence as:

“the logistic arm of the NHS; its task is to ascertain and to provide whatever supplies are legitimately required by the operational arm of the service for those who treat patients or are in ‘close support’ of them.”

Purchasing occurs at all levels in the NHS, from the hospital to the health department. Most of these contracts are “call-off’ arrangements, ie not based on fixed quantities. About 25% of the NHS revenue expenditure on goods and services is arranged under central contracts placed by health departments or by using contracts arranged by other government departments. Many other items are bought on bulk contracts arranged by the supplies organisations of health authorities. The value of these latter contracts now exceeds 30% of total NHS expenditure on supplies.

21.46 The health departments involvement in equipment and supplies differs in the four parts of the UK, although the DHSS takes the leading role on general purchasing policies. In Scotland the SHHD has no executive responsibility for contracts and its role is confined to ensuring that government policy is followed, that resources are used efficiently and economically and in determining policy on equipment, research, development and evaluation. The Welsh Office monitors purchasing. Central executive functions are undertaken by the supplies divisions of the Common Services Agency in Scotland and the Welsh Health Technical Services Organisation in Wales. The arrangements for central purchasing in Northern Ireland are very similar to those in Scotland with the Central Services Agency having executive functions.

21.47 Supplies organisation and policies in the NHS have been extensively Most recently a working party chaired by Mr A J Collier reported in 1976 on “Buying for the National Health Service”. Its main recommendation was that a “limited list” approach to medical equipment should be developed, “subject to the institution of adequate facilities for evaluation and acceptability to the users”. We understand that this proposal has met with opposition from some health authorities and the industries supplying the NHS. A supply board working group under the chairmanship of Mr B Salmon reported in 1978 on the arrangements for procuring NHS supplies (but not those related to the family practitioner service). The Salmon working group recommended that supplies policy should be determined at AHA level and that a supply council should be established as a special health authority whose policy decisions should be binding on DHSS and on health authorities. Its main functions would be to formulate policy at health department, region and area level; to arrange for the production and introduction of a comprehensive and universal computer based supplies information system; and to establish policy for the evaluation of the equipment and supplies used in the NHS.

21.48 Professor Perrin’s report recommended that:

“health departments should further encourage health authorities towards an early change-over to the use of central stores, where this has not yet been done, and also that NHS authorities should give urgent attention to improving stores management and control systems . . . additional staffing and training, and improved systems should be provided for central purchasing functions just as quickly as resources permit.”

21.49 Our interest in these questions is principally to ensure that resources in the NHS are used in an efficient and effective way. The NHS is a major purchaser of supplies and equipment and the problems of supplies policy appear to have been thoroughly researched in recent years. There is obviously a need for better specification of equipment required, improved arrangements for research, development and evaluation of new equipment, and more effective ways of ensuring that users are aware of the results of evaluation. At regional level there should be provision for an equipment information and advisory service. Some pieces of machinery are now enormously expensive and the cost of housing and using them may also be very large. It is essential therefore that they be evaluated before they are brought into general use. This should be a health department responsibility, and accepted by the health authorities as such; but at present the health authorities can buy any item of equipment, however expensive, which they can afford. We were disturbed to hear that whole body scanners, which can cost £0.5m to buy and £40,000 per annum or more to run, had been purchased by health authorities before they had been properly clinically tested and their uses and running costs ascertained. The Collier suggestions for a “limited list” would obviously be useful in this context and we recommend that the main proposals of the Collier report be implemented as quickly as possible.

Budgets and incentives

21.50 There are formidable obstacles to the efficient use of resources in the health service. The individual patient will gain little if he uses the service more The information necessary to monitor and evaluate decisions taken may not be available. Responsibility for expenditure may not fall on those who actually control the use of resources and there are few incentives for efficiency. If budget holders manage to achieve economies they are likely to find that their budget next year has suffered a corresponding cut and the savings used to cover expenditure elsewhere in the health service. A selfless concern for the generality of tax payers and patients is an insubstantial basis for efficient resource allocation. It is too easily turned into apathy, even cynicism by seeing others acting wastefully.

21.51 The weakness of financial management cannot be remedied without a clear agreement on what tasks should be carried out, some ranking of priorities and enforcement of budgetary discipline. In this respect it is interesting that we heard NHS administrators and treasurers welcome the introduction of cash limits because these made authorities decide on priorities

and enforce economies.

21.52 We attach great importance to improving incentives to NHS service providers to use resources effectively. We would like to see budget holders permitted to keep and spend as they think best within the service a proportion of any savings they may achieve and possibly be allowed to carry over a greater proportion of funds from one budget period to the next. We recognise that there are difficulties in arranging this: the efficient unit may be penalised because there is little scope for economy while the inefficient unit benefits, and measures of service output have to be developed to ensure that savings do not arise merely from a reduction in service provision or quality. However, schemes of this kind have been tried in the NHS, and we recommend that they should be encouraged.

Clinicians and resource management

21.53 The clinical decisions that doctors make heavily influence NHS expenditure. GPs prescribe great quantities of drugs and decide whether to refer patients to hospital. Hospital doctors decide whether to admit patients or treat them as outpatients, whether to order diagnostic tests, to prescribe or recommend surgical, pharmaceutical or nursing treatment, and when to discharge their patients. A doctor has clinical responsibility but is not usually accountable for the resource and financial implications of his decisions. No doubt many doctors are cost-conscious and careful, but the individual doctor normally has no direct incentive to economy. Doctors also need information about costs if they are to be cost-conscious. Apart from the expense of new equipment which they may request, they are often in the dark about the financial aspects of their work. They are told neither their unit costs nor the cost of the investigations and tests which they use. Some information about drug costs is made available to them but in no systematic or emphatic way. Much more could and should be done to inform them. The Perrin Report recorded that:

“Amongst health service finance staff, it is generally considered that the best way to encourage redeployment of resources . . . and also the best way to encourage cost consciousness more generally amongst medical staff, is to involve clinicians more positively in the managerial dimension of financial control . .. the key to the feasibility of this development is the willingness of clinicians to become involved, firstly in the resource allocation process, and secondly in the responsibility for, and ‘control’ of, resource spending/consumption for/by their specialties”

21.54 One way of involving doctors in the resource allocation process is to make them budget holders and thus accountable for the expenditure generated by their decisions. This approach was supported by the King’s College Hospital Group Medical and Medical Executive Committees who told us:

“More autonomy needs to be granted to each hospital or hospital group in order to redevelop local pride and encourage economy and good housekeeping. Financial autonomy for Divisions or Departments with allocation of Unit Budgets could, by freeing doctors to decide and finance their own priorities, bring a greater sense of responsibility in the individual use of taxpayers’ money with saving to the country at large, and benefit to patients in hospital served communities.”

21.55 There are considerable practical difficulties in clinician budgeting to be overcome and some doctors may see it as restricting their clinical freedom. It is worth stating, therefore, that there can be no such thing as absolute clinical freedom. A doctor must exercise his judgement as to which of the best available courses should be taken, but there will continue to be, as there is now, a limit on the courses available. As medicine becomes more technically advanced and expensive, the limitations on its practice are likely to increase. By becoming explicit resource managers doctors would gain a greater measure of control over their work within clearly defined resource constraints. We recommend that experiments with clinician budgeting should be encouraged.

Information

21.56 The best use of the resources of the NHS requires that its decision-makers be provided promptly with relevant information on needs and on the volume and cost of resources used in meeting those needs. Unfortunately the information available to assist decision-makers in the NHS leaves much to be desired. Relevant information may not be available at all, or in the wrong form. Information that is produced is often too late to assist decisions and may be of dubious accuracy.

21.57 Without explicit measures of the need of groups of patients for health care rational decisions on priorities and geographical distribution of resources are impossible. The lack of outcome measures means that judgements of the efficiency of service delivery rest on insecure foundations. Professor Perrin concluded that health authorities are:

“not well served by their information systems in monitoring their own progress; in particular, the data on patients are poor . . . and the financial control system does not show care groups used in planning, nor report output.”

21.58 If an organisation cannot keep track of its resources it is unlikely to be using them effectively and decisions on how those resources ought to be developed are made much more difficult. We were dismayed by the lack of information on the physical capital of the NHS. Professor Perrin’s report noted that:

“Another criticism levelled at the information system was the almost total lack of reliable data concerning the type, cost, age and location of equipment in everyday use. Without such data it was difficult to implement a planned replacement programme or to ensure the maximum utilisation of resources.”

21.59 Sensible decisions at all levels in the service require information on the costs of resources used in providing services to patients, but Professor Perrin’s team found that:

“The existing system of annual financial accounts (and linked functional ‘cost accounts’) do not appear to provide significantly-valuable information for improved resource allocation or other decision making . . . Cost data necessary for planning, decision making and resource allocation are difficult to derive. Important decisions have to be taken with only approximate knowledge of their cost . . . ”

21.60 We have urged the importance of improving the information available to decision makers in the NHS in a number of places in our report. We also support the sensible recommendations contained in Professor Perrin’s report. In particular we feel that it is essential that information on costs must be improved and costed options considered if the best use is to be made of the service’s resources. Improvements in information will initially require additional expenditure on administration but we would expect that the quality of decision making would thereby be much improved.

Family practitioner services

21.61 The family practitioner services (FPS) account for about £l,800m, or over one-fifth of all NHS expenditure. About half of this is spent on pharmaceutical services, mainly on drugs and dressings. Unlike the rest of the NHS the FPS are not subject to cash limits, except for the small expenditure on administration. The bulk of expenditure incurred in the services is automatically reimbursed by the health departments. The open-ended budget of the FPS was defended by the BMA on the grounds that:

“there is no way of controlling absolutely the amount of illness or disease and while it is possible, for example, to defer many surgical operations for 6 months or a year because of limited resources, similar action cannot be taken in the field of general medical care.”

21.62 Although the FPS are “demand determined” this does not mean that their expenditure cannot be forecast and influenced and hence budgeted The level of remuneration of doctors, dentists, pharmacists and opticians is subject to the ultimate control of the government; prices of drugs and optical appliances are subject to price control and negotiation; and there are arrangements for vetting the prescribing habits of doctors and the treatment given by dentists in the FPS. Prescribing, dental and optical charges have been used to control demand. In the past FPS expenditure has tended to rise more slowly than that of the NHS as a whole, though this trend has been reversed in the last few years.

21.63 The open-ended nature of FPS expenditure has disadvantages. First, the FPS is shielded from the effects of financial stringency, and the burden of any cut-back in NHS expenditure falls on the hospital and community services. This may accord with spending priorities, but it would be preferable if it were the result of an explicit decision rather than the accidental effect of a particular method of budgeting. It may encourage the misallocation of resources. Second, finance cannot be readily used to remedy geographical inequalities in the FPS. Third, and perhaps most important, the separate FPS budget does nothing to encourage joint planning of FPS and hospital and community services.

21.64 In Chapter 20 we recommended that family practitioner committees should be abolished and family practitioners contracted to health authorities in England and Wales as they are in Scotland and Northern Ireland. The closer involvement of the FPS in health service planning and decision making that this will imply might be further assisted by the FPS being covered by the same budget as the hospital and community services. However, there are some obvious practical problems to be overcome and we recommend that a study of the desirability and feasibility of a common budget for the family practitioner and hospital and community services should be undertaken.

Capital

21.65 Our recommendations in Chapter 10, if adopted, will lead to a significant increase in capital expenditure in the NHS. In 1978/79 this was running at the rate of about £460m per year or some 5.7% of total NHS expenditure. This is a considerable sum in itself but capital expenditure also has a profound influence on the pattern of revenue expenditure. It is therefore doubly important that capital projects are examined within a framework which is conducive to sensible decisions. This will require that alternative means of satisfying service objectives are systematically identified and all the significant costs and benefits of alternatives are considered explicitly. Many of the factors in investment decisions, particularly the benefits, are difficult or impossible to quantify or evaluate so that such decisions will continue to depend heavily on

professional judgements. However, as Professor Perrin’s team noted, it is important that a procedure should be adopted which:

“focuses attention on the desirability of making implicit policy judgments explicit, and ensuring that all can see clearly just what decision has been made and why.”

We understand that DHSS is considering how best to issue guidance, in consultation with health authorities, on the planning and appraisal of investment decisions. We welcome this approach and hope guidance can be issued swiftly to encourage rational appraisal of capital expenditure.

21.66 Capital expenditure in the NHS is controlled by the earmarking of capital funds in health authorities’ allocations. Greater flexibility between capital and revenue funds has been introduced in recent years. Professor Perrin’s team reported that:

“The consensus view within the authorities studied was that the separation between revenue and capital monies (limited virement notwithstanding) was not conducive to the proper (ie economic) evaluation of the choice between consumption and investment.”

The Regional Treasurers considered that RHAs were better able than DHSS to make the decision on the optimum mix of capital and revenue expenditure necessary to meet the service needs of the population they serve.

21.67 The Treasurers also considered that health authorities should be able to raise loans and service them from their annual allocations. The interest on such loans would bring home to users of capital funds the costs of their investment decisions and encourage a better balance between capital and other resources in the NHS. Access to the capital market would also enable health authorities to postpone or bring forward expenditure from one period to another.

21.68 These two questions are linked. One of the arguments against abolishing the distinction between capital and revenue is that in a centrally financed health service authorities might be tempted to spend on capital projects without taking full account of the revenue consequences. Exposure to the financial discipline of the capital market might solve this difficulty. A problem with giving health authorities access to the capital market is that they are not elected and publicly accountable bodies with independent revenue resources. Some authorities might be rated as worse risks than others and be faced with higher interest charges. This particular problem might not arise if health authorities were given access to an internal NHS capital market administered by the health departments perhaps along the lines of the borrowing and lending arrangements for temporarily surplus SHARE funds recently introduced in Scotland.

21.69 There are clearly potential disadvantages which may outweigh the theoretical attractions of charging interest on NHS capital funds, and Professor Perrin considered, and we agree, that detailed research would be needed before it could be considered a workable alternative to current methods of capital allocation. In the meantime health authorities can take advantage of the considerable degree of flexibility that has recently been introduced.

Conclusions and Recommendations

21.70 There is no objective or universally acceptable method of establishing what the “right” level of expenditure on the NHS should be. Some of our recommendations would increase NHS expenditure, but others should lead to On balance our recommendations will increase the cost of the NHS, but our judgement is that these additional resources will be justified by the benefits which will flow from them. We also consider it right that the nation should spend more on the NHS as it gets wealthier.

21.71 We made our own broad assessment of the financial implications of our recommendations, but in most cases we have not included them in our The accurate costing of any recommendation that affects the NHS in the four parts of the UK would be difficult enough if undertaken by the health departments themselves. For obvious reasons we could not ask them to do this exercise for us, and we had neither the time nor resources to make other than the most rudimentary estimates.

21.72 No method of financing a part of national expenditure as large and as politically sensitive as the health service is likely to remove it from government influence. Discussion of the merits of alternative methods of finance must therefore focus on their implications for the way the health service is organised and performs, rather than on the total amount of finance they will generate. We are not convinced that the claimed advantages of insurance finance or substantial increases in charge revenue would outweigh their undoubted disadvantages in terms of equity and administrative costs. The same disadvantages arise from the existing NHS charges.

21.73 The geographical distribution of the provision of health care has become fairer since the NHS was founded but there is still some way to go. It is essential that the resource allocation procedure adopted should be the subject of informed and public scrutiny and we welcome the recent change to explicit formulae based on estimates of need.

21.74 The system of financial management in the NHS does not sufficiently encourage efficient resource use. Much of the information required for effective management is not produced, or is inaccurate, or too late to be of value. Those held responsible for expenditure are often not in a position to control it. We commend Professor Perrin’s Report to the health departments.

21.75 We recommend that:

- it is for government to decide how the NHS should be funded, but there is a firm case for the gradual but complete extinction of charges (paragraphs 21.28 and 21.29);

- the health departments should prosecute the research necessary for improvement of the resource allocation formulae (paragraphs 21.41 and 42);

- there should be an explicit formula for the distribution of funds to the health service in the four parts of the UK (paragraph 21.43);

- the main proposals of the Collier report on equipment and supplies should be implemented as quickly as possible (paragraph 21.49);

- health departments should encourage experiments with budgeting (paragraphs 21.52 and 21.55);

- a study of the desirability and feasibility of common budgets for FPS and hospital and community services expenditure should be undertaken (paragraph 21.64).