Types of Approved Societies

49. The societies approved under these wide provisions are of every size and of many different types. They can be grouped under five main heads according to the kind of office or society with which they are associated, namely. Friendly Societies with branches. Friendly Societies without branches, Industrial Life Offices, Trade Unions and Employers’ Provident Funds. Friendly Societies, whether with or without branches, are engaged in the main in voluntary insurance against sickness on a mutual basis. But many or most of them, in addition to sickness benefits, give benefits for death or maternity, and recently they have undertaken a growing amount of endowment and deposit insurance. The Industrial Life Offices are engaged primarily in insurance for burial expenses and other expenses connected with death, but like the Friendly Societies have developed in the direction of general life insurance and endowment insurance. The work of these Offices is examined in more detail in Appendix D. The primary function of Trade Unions is in dealing on behalf of their members, with employers in regard to terms and conditions of work. But a large number of them also provide insurance benefits of various kinds for unemployment, sickness, old age and other contingencies; most, but not all, of the Trade Unions with which Approved Societies are associated have a friendly side. Employers’ Provident Funds are societies consisting of persons entitled to rights under superannuation or other provident funds established for the benefit of persons employed by one or more particular employers.

50. Under each of the five heads there are great differences both of size and of method. As a whole, the Approved Societies range in membership from under 50 up to the 3,000,000 of the National Amalgamated Approved Society associated with a group of Industrial Life Offices or the 4,000000 of the four technically separate societies associated with the largest of these offices – the Prudential Assurance Company, Ltd. The number of Approved Societies is about 800, but some of these have branches which are separate financial units; the total number of units which are valued separately and each of which, therefore, may give benefits differing from those of other units, is now about 6,600, a substantial reduction from the number at earlier valuations The reduction has been most marked among the Friendly Societies with branches, from about 15,500 units in 1912, to less than 8 500 at the first valuation in 1918, and about 5,700 at the fifth valuation in 1938*. Some of these societies, while retaining separate branches for their own benefits group the branches into larger units for administration of national health insurance thus diminishing the number of valuations and the chance that two members of the same society in different neighbouring branches may receive different rates of national insurance benefit.

51 The Approved Societies are formed on many different bases, some with trade or local associations, but many without. Even where a society starts with a definite local association its members may move so that any Approved Society may carry on business in any part of the country. In any moderate sized town the insured persons are likely to be scattered among some hundreds of societies and branches, each of which has to make arrangements for administration of cash benefits to members entitled to them. The Royal Commission of 1926 obtained information as to the numbers of separate societies functioning in several typical towns, and this information has been brought up to date for the present Committee. The numbers of societies in each of those towns in 1942, with the corresponding figures from the Royal Commission Report of 1926 given in brackets are as follows: in Liverpool 437 (488) societies had members ; in Bolton 248 (285) ; in Brighton 324 304), in Norwich 241 (213) ; in Reading 361 (245) ; and in Tynemouth 181 (168).

52 The membership of a particular society in a particular town is often very small Figures for some typical towns in 1941, with corresponding figures from the Royal Commission Report of 1926 in brackets are as follows: in Glasgow in 1942 out of 396 (384) societies, 97 (98) had each one member only; In Dundee, out of 219 (217) societies, 61 (52) had each one member, and another 54 (47) had each from 2 to 9 members. Almost any town would give similar results. The number and variety of administrative units functioning in each town is actually greater than is suggested by the above figures which relate to societies; some of these societies have branches which are financially separate. Though the number of financially separate branches of societies with branches is now only about a third of the original number, it still remains very large.

Distribution of Insured Persons by Societies

53. While in essentials the approved society system has remained the same as in 1912, there have been interesting changes in the relative importance of different types of society. In 1912, according to the not entirely adequate statistics which were compiled at the outset, the distribution of insured persons in Great Britain, according to the five principal types of Approved Society, was as follows :—

TABLE I

National Health Insurance—distribution or insured persons in Great Britain by type of approved society in 1912

| Type of Society | Men | Women | ||

| Numbers (in 000’s) |

Percentage Distribution |

Numbers (in 000’s) | Percentage Distribution | |

| Industrial Life Offices …Friendly Societies without branchesFriendly Societies with branches | 2,9712,1782,3481,15953 | 34-125-027-013-30-6 | 2,17264858725915 | 59-117-615-97-00-4 |

| Trade UnionsEmployers’ Provident Funds … | ||||

| total ………. | 8,709 |

100-0 |

3,681 | 100-0 |

54. The more precise statistics for later years, compiled in connection with the several valuations of Approved Societies, are not exactly comparable with those given above. The differences, e.g., the inclusion of Northern Ireland membership in the valuation statistics, affect particularly the actual numbers; the percentage distributions may be regarded as broadly comparable. The following statement gives the numbers and percentage distributions for the second valuation (corresponding to the year 1923) and the fifth valuation (corresponding to 1938):—

TABLE II

National health insurance—distribution of insured persons in Great Britain and Northern Ireland by type of approved society in 1923 and 1938

| type of society | Men | Women | ||||||

| Numbers (in 000’s) | Percentage Distribution | Numbers (in 000’s) | Percentage Distribution | |||||

|

1923 |

1938 |

1923 |

1938 |

1923 | 1938 |

1923 |

1938 |

|

| Industrial Life Offices Friendly Societies without branches …….. Friendly Societies with branches …….. Trade Unions .. Employers’ Provident Funds |

3,810 2,540 2,390 1,270 80 |

5,120 3,470 2,230 1,190 50 |

37-7 25-2 23-7 12-6 0-8 |

42-5 28-8 18-5 9-8 0-4 |

3,060 1,010 760 240 30 |

3,350 1,67077029030 |

59-9 19-9 14-8 4-8 0-6 |

54-7 27-3 12-7 4-7 0-6 |

| Total |

10,090 |

12,060 |

100-0 |

100-0 |

5,100 |

6,110 |

100-0 |

100-0 |

These figures snow a steady increase both in the number and in the proportion of insured men covered by the Industrial Life Offices and by the Friendly Societies without branches. In the case of women, however, the Industrial Life Offices have a declining proportion of the whole (though their women’s membership has actually increased), whereas the Friendly Societies without branches have substantially increased their proportion of the female insured population. Taking men and women together, the Industrial Life Offices had nearly 42 per cent, of the total membership in 1912, and had nearly 47 per cent, in 1938; the Friendly Societies without branches had 22 per cent, of the membership in 1912 and had more than 28 per cent, in 1938. Taking these two types of centralised societies together, they accounted for about 64 per cent, of the total men’s and women’s membership in 1912, nearly 69 per cent, in 1923 and practically 75 per cent, in 1938. The two other principal types—Friendly Societies with branches and Trade Unions—each have a steadily declining proportion of the whole membership. They accounted for 35-2 per cent, of the insured population in 1912, 30-7 per cent, in 1923, and only 24-6 per cent, in 1938. It seems safe to say that of the total increase in the insured membership in Britain between 1912 and 1938 (probably about 5,400,000), practically the whole has taken place in the Approved Societies associated with Industrial Life Offices or with the Friendly Societies without branches. The other three groups—Friendly Societies with branches, Trade Unions and Employers’ Provident Funds—have been retrograde or stationary.

55. Looking at the position in 1938, and taking men and women together, of the 18,170,000 insured persons who were members of Approved Societies, 8,470,000 or 46-6 per cent, were in Approved Societies associated with Industrial Life Offices; 5,140,000 or 28-3 per cent, in Friendly Societies without branches; 3,000,000 or 16-5 per cent, in Friendly Societies with branches; 1,480,COO or 8-1 per cent, in Trade Union societies ; and 80,000 in Employers’ Provident Funds.

Additional Benefits

56. The essence of the approved society system is financial responsibility; each society can realise a surplus or a deficiency for its members out of the administration of the contributions collected compulsorily from them. After each quinquennial valuation, surpluses, after retention of suitable reserves, are distributed in additional benefits. A deficiency means that the society can give no additional benefits; deficiencies are in practice made up from a central pool reserved for that purpose from the contributions. The finance of the national health insurance scheme has been such as to yield surpluses in societies covering a large proportion of the whole insured population. At the fifth valuation, relating approximately to 1938, additional benefits were made available in societies with about 88 per cent, of all insured men and 81 per cent, of all the insured women ; that is to say, only 12 per cent, of the men and 19 per cent, of the women had no more than the statutory benefits.

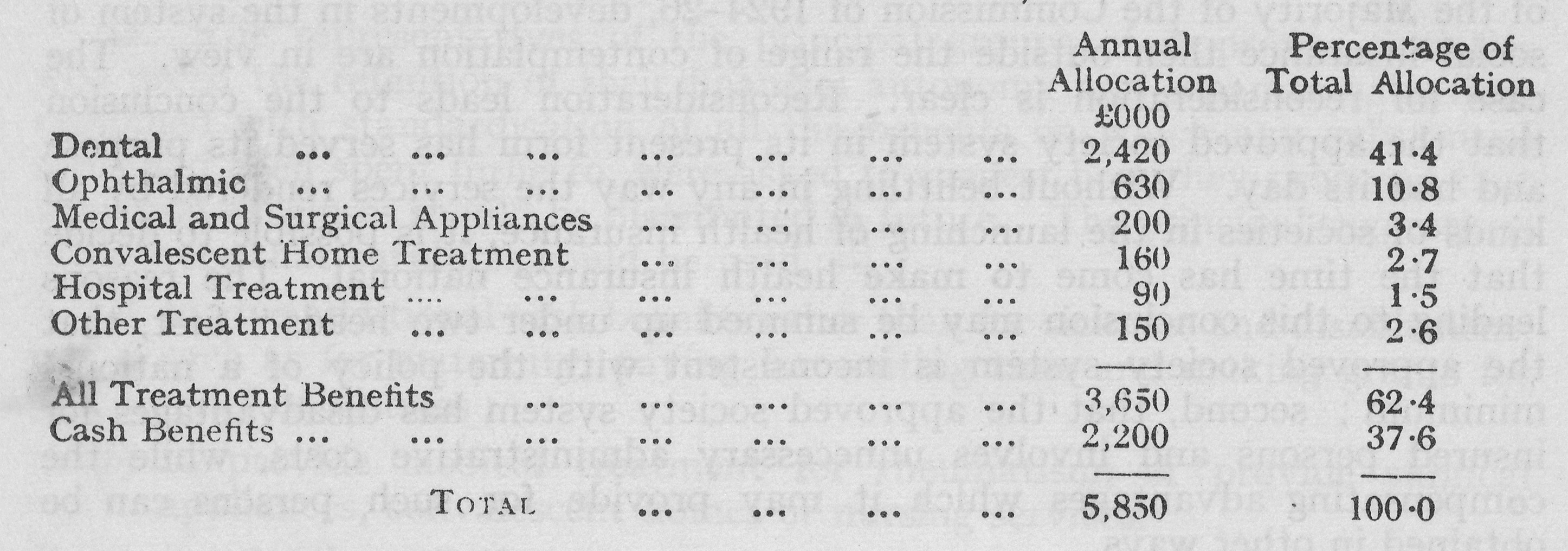

57. The surpluses were very substantial in amount, as well as in the numbers covered. The annual allocation in schemes adopted on the fifth valuation amounted to £5,850,000 as compared with a total expenditure on benefit of all kinds, including additional benefits, of about £35,000,000. The distribution of this total of £5,850,COO between different purposes is shown in the following table :—

TABLE III

The cash benefits at £2,200,000 represent 37-6 per cent, of the whole allocation. Additional sickness and disablement benefits were given in societies containing 63 per cent, of all insured men, but only 28 per cent, of the spinsters and widows and 20 per cent, of the insured married women. That is to say, while rather over one-third of all the insured men got no more than the statutory sickness and disablement benefit, three-quarters of all the insured women were in the same position. The average weekly addition to sickness benefit in societies giving such an addition was 3.2s. for men and 2.2s. for women, but these averages, particularly for men, cover great differences in the actual addition. The additional sickness benefit ranged from 1/- a week to as much as 15/- a week, though this last is an abnormal figure applying only to a few hundred persons; less than 3 per cent, of the men and practically none of the women received an increase of more than 5/- a week.

58. Of the £2,200,000 allotted to additional cash benefits about £250,000 was for maternity and practically the whole of the rest was for sickness or disablement. Of the money allocated to treatment benefits an overwhelmingly large proportion, more than four-fifths, was devoted to dental and ophthalmic benefit. Most of the remaining one-fifth of the money for treatment benefits was devoted to the provision of medical and surgical appliances, convalescent homes and hospital treatment.

Views of Royal Commission of 1924-26

59. The approved society system was examined at some length by the Royal Commission of 1924-26. The majority of the Commission, after considering a variety of criticisms, concluded that the Approved Societies should be retained as an essential part of the health insurance scheme and submitted a recommendation to that effect. They added that ” it must be clearly understood that our recommendation is made in relation to the scheme of National Health Insurance as it exists at present, and that our view in favour of the retention of Approved Societies does not necessarily imply that developments in the system of social insurance outside the range of present contemplation might not necessitate a reconsideration of the position.” (Royal Commission on National Health Insurance, 1926. Majority Report, para. 223.) The Minority of the Commission took the opposite view. They held ” that it is undesirable to retain Approved Societies any longer as the agencies through which benefits paid in cash are distributed to insured persons ” and recommended ” that Local Authorities could and should take the place of Approved Societies as the Authorities through whom sickness and disablement benefits should be administered.” ( Royal Commission on National Health Insurance, 1926. Minority Report, paras. 3 and 7.)

60. Today the question comes up once more at a time when, in the words of the Majority of the Commission of 1924-26, developments in the system of social insurance then outside the range of contemplation are in view. The case for reconsideration is clear. Reconsideration leads to the conclusion that the approved society system in its present form has served its purpose and had its day. Without belittling in any way the services rendered by all kinds of societies in the launching of health insurance, it is possible to decide that the time has come to make health insurance national. The reasons leading to this conclusion may be summed up under two heads: first, that the approved society system is inconsistent with the policy of a national minimum ; second, that the approved society system has disadvantages for insured persons and involves unnecessary administrative costs, while the compensating advantages which it may provide for such persons can be obtained in other ways.

Approved Society system inconsistent with the policy of a national minimum

61. If the Approved Societies are to have responsibility for administering cash benefits for sickness and disablement, they must be independent financially and have the possibility of giving or withholding according to their financial results, additional benefits, which must both be so valuable that it is right to spend upon them money collected compulsorily and at the same time not so important that they ought to be available for every insured person. These additional benefits must either be cash benefits or treatment benefits.

62.As regards cash benefits, with two exceptions, all the organisations directly concerned in the administration of national health insurance which gave evidence to the present Committee, including the National Conference of Friendly Societies, the National Conference of Industrial Assurance Approved Societies, the Prudential Assurance Company Limited, the Trade Union Approved Societies, the Association of Approved Societies, and the National Union of Holloway Friendly Societies, agreed in recommending that Approved Societies should no longer have power to add to the statutory sickness and disablement benefits ; the societies represented by these organisations include over 90 per cent, of the 18,000,000 members of Approved Societies. The only organisations which gave evidence in a contrary sense were the National Federation of Employees’ Approved Societies, representing about 300,000 insured persons, and the National Federation of Rural Approved Societies, representing about 400,000 insured persons. This nearly unanimous agreement of the various groups of Approved Societies for the abolition of the principal additional cash benefits is clearly in accord with the general sentiment of insured persons and the development of social policy. It is felt to be inequitable that for uniform contributions under a national scheme different rates of cash benefit should emerge. If the State provides a minimum statutory benefit based upon assumed subsistence needs, it is felt to be anomalous that from contributions collected for these purposes particular groups should be able to secure benefits above that minimum. As regards treatment, to provide any form of treatment as an additional, rather than as a statutory benefit, means that it is given selectively, with reference not to the degree to which it is wanted but according to valuation results. An overwhelmingly large proportion of the valuation surpluses devoted to treatment benefits in the past has been allocated for the provision of dental and ophthalmictreatment, showing a need for these services which led all the associations of Approved Societies which gave evidence to the present Committee to recommend that these particular forms of treatment should be made available for all insured persons.

63. The representatives of the principal groups of Approved Societies who urged the retention of their financial autonomy and separate valuation, combined with standardisation of all the benefits on which any substantial sums had been spent hitherto, were asked to suggest how they proposed that valuation surpluses should be distributed in future. The principal suggestions made were that surpluses could be used:—

(a) to give additional cash benefits other than for sickness and disablement, such as for maternity, paying for waiting time and making grants for relief of distress;

(b) to provide medical treatment for rheumatism, or provide surgical appliances, convalescent homes or nursing services.

It is unlikely that all these suggestions together would make it possible to dispose with advantage of anything like the surplus which would be realised by some societies, if the present system were retained. Most of the organisations representative of Approved Societies which gave evidence to the Committee recognised that their proposals for standardising the principal cash benefits and for making statutory the principal treatment benefits involved further pooling of surpluses between societies. Eighty-five per cent, of the very substantial annual sum (about £5,850,000) allocated for additional benefits on the last valuation was devoted to the provision of benefits—sickness, disablement, dental and ophthalmic—which in the opinion of practically every one who gave evidence to the Committee ought now to be made statutory and universal. With the raising of the rates of contribution to provide the subsistence minimum in all cases, the surpluses of the more fortunate societies will be increased proportionately. But, apart from this practical difficulty of finding a means of disposing of surpluses which must remain large in total if they are to give an adequate motive for economical administration, the more serious objection of principle remains. Why should treatment for rheumatism, why should surgical appliances, convalescent homes and nurses be reserved for those classes of the community which are already the most healthy, and denied to others, by the results of a valuation surplus? Why, if adequate maternity grants are important, should they be given selectively? If the State, as a general principle, lays down one provision as to waiting time, why should that be modified for a particular group of individuals? Once it is accepted that prolongation of illness means need for at least as much income, and not for less income, than at the beginning of illness, a policy of enabling persons with low risks of illness to get for their shorter periods of illness higher cash benefits or better treatment than those with less favourable sickness experience, becomes indefensible in a national insurance scheme.

Disadvantages to insured persons of approved society system

64. Apart from inequality of benefits, the approved society system has five principal disadvantages for insured persons:—

(1) The Approved Societies are of every size and sort. Insured persons are continually liable to change their place of work and residence. Unless, therefore, an insured person belongs to one of the larger societies with agencies everywhere, he has no assurance of any personal treatment or contact, if he has to move his residence.

(2) Maintenance of the approved society system, involving separation of responsibility for ordinary sickness from responsibility for industrial accident and disease or for unemployment, involves, by consequence, maintenance of the conflict of interests between different administrative authorities, each rightly endeavouring to reduce charges on its own fund, and referring any doubtful claims to some other agency.

(3) Maintenance of the approved society system involves maintenance of different procedures for determination of claims, different and often not well-known routine as to appeals, and different principles of decision.

(4) The approved society system, as explained in para. 43, requires either the keeping of separate contribution cards for health and unemployment insurance or special machinery for assigning health contributions to particular societies. Whichever method is adopted, there must be a separate valuation every five years of each of the financial units, now numbering about 6,600. Whether through duplication of insurance documents or through the setting up of alternative machinery, additional cost and trouble to all parties is involved, not for the purpose of enabling insured persons to pay for additional insurance, but in order to enable particular groups of such persons to obtain larger or smaller shares of a fund to which all alike have contributed compulsorily.

(5) No organised disinterested information is available to guide insured persons in the choice of an Approved Society, and no such information could be provided by any official or semi-official body, since this would mean favouring some societies and appearing to criticise others. Officially, all the societies must be allowed to compete for members on equal terms, and the insured persons must make their choice—which may affect their benefits very substantially over long periods of time— without systematic guidance or any easy means of comparing different societies.

65. Some of these disadvantages have become apparent only in the course of time. If they had all been realised in 1911, it might still have seemed worth while to adopt the approved society system at the launching of national health insurance. The system made it possible to build State insurance upon the foundations of voluntary insurance, and brought to the service of the community in a wider field the experience and the organisation of the great friendly society movement. There was no suggestion, at that time, that State insurance of itself should give benefits up to subsistence level, that is to say, there was no policy of a national minimum; the benefit provided when the approved society system began was 10/- a week for men and 7/6 a week for women for 26 weeks of sickness, and 5/- a week thereafter.

New basis for co-operation between state and friendly societies

66. Today, views on social policy differ in two respects from those accepted in 1911. There is wide-spread acceptance of a principle of a national minimum. There is growing support for the principle discussed in paras. 24-26 that in compulsory insurance all men should stand in together on equal terms, that no individual should be entitled to claim better terms because he is healthier or in more regular employment. With both these principles the approved society system, in its present form, is in irreconcilable conflict. If the combination of State insurance and voluntary insurance against sickness which was the corner-stone of the plan of 1911 is to be retained, it must be on a different basis. The attempt to find such a basis is well worth making for several reasons. As against the disadvantages named above, it can be claimed that two advantages are secured by the approved society system to the insured person. First, if in addition to the benefits of compulsory insurance he wishes to increase his provision against sickness by voluntary insurance through a society giving sickness benefit, it is possible for him now to obtain both the compulsory and the voluntary benefit through the same source. Second, combination of compulsory health insurance with voluntary insurance for other purposes, such as sickness benefit through a Friendly Society or Trade Union or funeral expenses through an Industrial Life Office, may make it possible for the combined insurance to be administered at lower cost than if each was dealt with by a separate organisation; there is here a possible saving to set against the additional administrative cost of the approved society system.

67. Each of these possibilities is a real advantage secured today under the approved society system, though neither is of first-rate importance, or comparable to the disadvantages. If both had to be sacrificed in making national health insurance truly national, the gain would outweigh the loss. But no such sacrifice is necessary. The first advantage, of enabling insured persons to obtain State and voluntary sickness benefit through the same agency, can be retained completely, and the second advantage, of possible administrative economy through combination of services, can be retained wholly or in large measure without maintaining Approved Societies as separate financial units giving unequal benefits in compulsory insurance. The purpose in view in giving each Approved Society its separate finance is to give it an interest in the results of its management. This is a necessary purpose; it would be impossible to entrust the administration of national sickness benefit to independent bodies under arrangements which did not make them feel direct responsibility for careful administration. But in the case of societies giving voluntary sickness benefit from their own funds in addition to benefits provided by compulsory insurance, it is possible to give a motive for care in administration in another way than that adopted in 1911. This other way depends on requiring the societies to expend money from their own funds in some reasonable proportion to the money which they pay as State benefit on behalf of the Social Insurance Fund.

68. This leads to a proposal that the Department concerned with social insurance—that is to say, the Ministry of Social Security—should be prepared to make arrangements with societies fulfilling certain conditions, under which these societies could act as responsible agents for the administration of disability benefit to their members. The conditions to be fulfilled by any society desiring to make an arrangement would include the following :—

(a) That it gave a substantial disability benefit from its own resources, i.e. from the voluntary contributions of its members.

(b) That it had an efficient system for sick visiting its members wherever they might be.

(c) That it was effectively self-governing.

(d) That it did not work for profit and was not associated with any body working for profit.

(e) That it was registered under the Friendly Societies Acts or the Trade Union Acts or if not registered that it conformed substantially to the requirements for registration.

How closely payment of State benefit would have to be associated with payment of voluntary benefit is a matter for further consideration. It does not seem necessary to require that for each individual payment of State benefit there should be a simultaneous payment of voluntary benefit; some general condition relating the expenditures on the two purposes should be sufficient to give the society a motive for careful administration of State benefit, and to make it possible to trust it as a responsible agent, taking decisions in individual cases,- subject only to general supervision. It would no doubt be necessary for the Ministry of Social Security, before making arrangements, to be satisfied that the voluntary side of any society desiring to administer State benefit had an adequate financial basis ; the prestige of being recognised as agent for the national scheme should not be used to attract voluntary contributions to an unsound society. But no question on this would be likely to arise in regard to most of the societies which might contemplate making arrangements.

69. By arrangements on the lines suggested above, even if the approved society system as such is ended, a responsible function in the administration of social security benefits can remain for societies which give sickness benefit of their own. This would secure the first of the advantages claimed above for the approved society system, and would secure the second advantage also so far as the members of these societies are concerned. Most of these members would not notice any difference between the present system and what is now proposed, except in higher benefits. The proposal has other objects even more important. One is to enlist the help of the Friendly Societies in ensuring that individual problems are handled with local knowledge and that the general welfare of sick persons, as well as provision of cash benefits, receives adequate consideration. The second object is that of encouraging voluntary insurance to supplement the subsistence benefits provided by compulsory insurance. With this in view, it might well be provided that societies making arrangements as proposed, should be allowed to recruit juvenile members for State benefits only, with a view to their subscribing for voluntary benefits on becoming adults.

The problem of industrial life offices

70. Arrangements on these lines could be made with Friendly Societies and with Trade Unions giving friendly benefits. They could not be made with bodies like the industrial assurance companies and collecting societies, in which the administration of health insurance is now associated, not with the payment of voluntary sickness benefits, but with industrial assurance, that is to say, life assurance through collectors. It is not easy, indeed, to see how supersession of Approved Societies as separate financial units, with a view to standardisation of adequate benefits both of cash and of treatment, can be combined with giving to the Industrial Life Offices in their present form any continuing association with the administration of health insurance. To say this is not to belittle the service rendered by these offices in the past, in providing efficiently and on reasonable terms the machinery of health insurance for the large numbers of insured persons who were not members of Friendly Societies; this service was acknowledged in emphatic and generous terms by the originator of national health insurance in 1933. But this service to national health insurance is directly associated with the purpose of securing customers for industrial assurance, and has undoubtedly been of great advantage to the Industrial Life Offices in the extension of their business. Whether or not this association of social insurance with private business was necessary or desirable in the past, there can be no justification for continuing it in the future, under a system of uniform adequate benefits for disability. It is impossible to contemplate an arrangement under which bodies working for private profit were allowed to act as agents of the Social Insurance Fund at the risk of the Fund, and to use this agency as a means of extending their business; on these terms the Industrial Life Offices, so far from having any motive for careful administration of disability benefit, would have a direct economic motive to be liberal with the money of the Social Insurance Fund, in order to obtain or retain customers for industrial assurance and to increase the profits of their shareholders or the pay of their staff. ..The third and

fourth of the conditions suggested above for societies desiring to make agency arrangements are fundamental.

71. If the facts of the situation are faced, it becomes clear that for the future of national health insurance there are three possibilities alone:

i) to keep the approved society system with substantial inequalities of benefit and therefore with substantial inadequacy of benefit, either of cash or of treatment, for those who are not fortunate in their society ;

ii) to break the association established in 1911 between national health insurance and industrial assurance, extending now to nearly half the insured population;

iii) to convert industrial assurance itself from a competitive business into a public service. The first possibility should by now be regarded as excluded by argument and evidence. The choice between the second and third possibilities depends upon many considerations, some of which are unconnected with health insurance; they are discussed in Change 23 below and in Appendix D, and reasons, both of public policy and of administrative convenience, are given for preferring the third. Not the least of the reasons is that this third course, more fully than any other course, would make it possible to retain for the service of insured persons the organising ability and the experience of the staff of all grades who now serve the Industrial Life Offices.

72. As is shown above, there is no need, in ending the present approved society system, to break or even to weaken appreciably the close relation that has existed hitherto between the administration of State insurance for sickness and of voluntary insurance for the same purpose. If the reasons given for bringing the approved society system as such to an end are accepted by the Government and Parliament, it is to be hoped that those voluntary organisations with which the arrangements suggested could appropriately be made will be willing to join in them and to continue to serve the people both in voluntary and in State insurance. But these arrangements, though desirable, are not an essential part of the scheme. If it should appear to the Friendly Societies and Trade Unions that, under the new scheme of social security, they could serve their members best by confining themselves to voluntary insurance, managing their own affairs only and not those of the State as well, they would be free to take this course. In that event, in place of the suggested arrangements there would be no difficulty in organising, for these members and for all other insured persons, decentralised administration of disability benefit as part of the work of the Ministry of Social Security, taking over whatever staffs were available for this purpose from Approved Societies of every type ; there are arguments, on merits, for making sick visiting a unified national service, as it is in effect in Northern Ireland, and in associating it with nursing service. The suggestion made for arrangements with Friendly Societies and Trade Unions giving sickness benefit to replace the present system of Approved Societies, and to continue in substance under a slightly different form, the association of these organisations with State insurance, is eminently desirable. But it is not essential in the Plan for Social Security, and if for any reason it does not commend itself it can be omitted, in favour of national administration throughout of a national service. It is included, therefore, as one of the bracketed proposals of the Report.

73. In any case there is no reason for the State to enter directly or in directly the field of voluntary insurance against sickness. Voluntary insurance to supplement compulsory insurance is an integral feature of the Plan for Social Security, and there are other fields in which direct State action may be needed for control or development of such insurance, but this particular field of voluntary insurance against sickness is covered adequately., and on right principles by the Friendly Societies, with their long traditions of disinterested service and brotherly co-operation. It can be left safely in

their hands.

Views of organisations giving evidence

74. Abolition of the present system of Approved Societies with separate finance and giving unequal benefits for compulsory uniform contributions was recommended by the great majority of the bodies that expressed views on the system to the present Committee. These bodies included the Trades Union Congress General Council, and the Scottish Trades Union Congress; all other organisations of employees which submitted memoranda or gave evidence, such as the National Union of Railwaymen and the National Association of Local Government Officers; the only employers’ organisation which made definite recommendations on the general problems before the Committee, namely the Shipping Federation; and the National Council of Women. The various associations of Local Authorities, including the Association of Municipal Corporations, the County Councils Association and the Association of County Councils in Scotland, recommended a comprehensive and unified scheme of social insurance and assistance and either by inference or specific reference envisaged the supersession of Approved Societies as separate financial and administrative units. Similar views were expressed by the bodies devoting themselves to the stud}’ of social problems, such as Political and Economic Planning (P.E.P.) and the Fabian Society ; the former of these argued that public administration could provide a much simpler, cheaper and more constructive type of service ; they said that for the great majority of insured workers an Approved Society is not a society at all; it is not an association of members for mutual aid with any kind of corporate spirit or social life, but merely a complicated system of book-keeping and of officers who pay out or withhold benefits.

75. Abolition of the approved society system was accepted as necessary to a national scheme of unified insurance by two of the smaller groups of Approved Societies—namely the Association of Approved Societies and the Trades Union Approved Societies. It was opposed only by the remaining groups of societies concerned with the administration of health insurance; these include the National Conference of Friendly Societies, the National Conference of Industrial Assurance Approved Societies, the societies associated with the Prudential Assurance Company, and the National Federation of Employees’ Approved Societies. The first three of these, as stated, recommended standardisation of all the principal benefits, whether of cash or of treatment, given hitherto. On the view taken in this Report, this involves seeking some other basis than the present one—of financial autonomy and separate valuation of Approved Societies—for continuing the association of these organisations with the administration of national insurance. This basis can be found by arrangements on the lines suggested above for the Friendly Societies and Trade Unions giving sickness benefit. It can be found for the Industrial Life Offices by converting them into a public service.

76. At the introduction of national health insurance, recourse to the device of Approved Societies was natural. It made possible full utilisation in this field of the ‘magnificent pioneer work of the Friendly Societies. By enlisting the business motive, energy and organisation of the Industrial Life Offices, it ensured that the machinery for dealing with the new masses brought into insurance for the first time, was available at once wherever there was need. But it did so at the price of including now nearly half of the insured population in Approved Societies which cannot by any stretch of the imagination be described as under the absolute control of their members and which, though making no profit—perhaps even a loss—themselves, are in effect governed by the profit motive either of the offices with which they are associated or of their agents. The advantages of direct self-government in social insurance can indeed be bought too dear; the smaller the unit, the greater the reality of self-government, but the greater also the disadvantages of any change of residence or employment, such as may be forced on insured persons by economic circumstances. The history of the first thirty years of national health insurance, while it preserves many instances of lively democratic self-help in small societies connected with particular places or trades, shows also an unmistakable general tendency towards larger units of administration. The evidence given to the present Committee presents an overwhelming consensus of public opinion that equal contributions to a national scheme of insurance should lead to equal rates of adequate benefit. Experience and evidence together point the way to making a single Approved Society for the nation. Examination shows that this can be done without losing any of the main advantages of the system of today or breaking the fruitful association between the State and the Friendly Societies that began in 1912.