We started off paying for the National Health Service via National Insurance Contributions in 1912.

Lloyd George’s slogan – 9d for 4d – was only the first of many attempts to pass off National Insurance as a pain free alternative to taxation. The impression was created that by paying contributions people were building up a fund which would entitle them to future benefits. It was very successful, and many people still believe it, but in reality it was, and is, a giant Ponzi scheme. Today’s contributions pay for the benefits paid out now.

“.. all the benefits in some sense are based on a pay as you go system, which is what the National Insurance system is. If you like, all the benefits are too easy. None of us has ever paid, or will ever pay, because even on the pension side it is not actuarially calculated, the full value of our benefits. This is a function of the inter-generation apportionment process whereby the working generation today basically pays for the pensions of the generation which has now retired and we go forward in the hope that each successive generation will, in return for something which is much less than full value, go on doing so.” (Treasury and Civil Service Select Committee: Structure of personal income taxation & income support – Minutes of Evidence 23 June 1982, 11 May 1983 HC 331-viii 1981-82 Qs 839-841 pp 398-9)

After 1948 there was no direct relationship between the payment of contributions and entitlement to the National Health Service, though that myth too is widely believed. Bevan pointed out in 1952 “Many people still think they pay for the National Health Service by way of their contribution to the National Insurance Scheme. The confusion arose because the new service sounded so much like the old National Health Insurance, and it was launched on the same date as the National Insurance Scheme.”

The contributory principle has considerable political force:

“People are prepared to subscribe more by way of contributions, which they see as offering returns in the form of personal and family security, than they would be willing to pay by taxation, which might be diverted to a wide variety of uses. They are led to believe that because of their contributions to the scheme they are participating in its administration and may thus exercise political control over its development.” (Ogus, Barendt & Wikeley, The Law of Social Security, 5th edition 2002 p29)

There is a direct contribution from National Insurance Contributions to the financing of the NHS, but it is modest – £21 billion in 2014/15, about 20% of NHS expenditure.

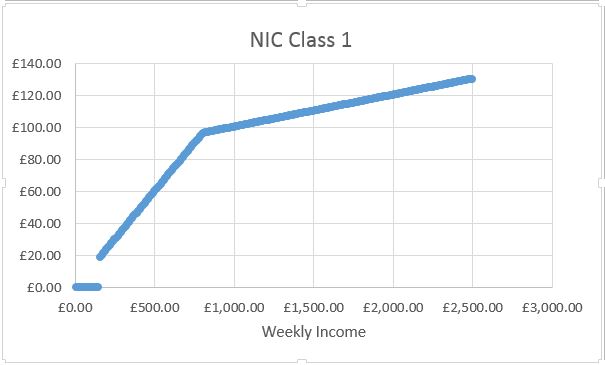

The Blair government raised National Insurance Contributions in the 2002 budget. For employees the rate of NICs rose by 1% to a rate of 11% on all earnings between the primary threshold and the Upper Earnings Limit (now £805 per week) – and a new 1% rate was charged on earnings above the UEL. For employers the rate of NICs rose by 1 percentage point to a rate of 12.8% on earnings above the secondary threshold (now £153 a week). For the self-employed the rate of NICs rose by 1 percentage point to a rate of 8% on all earnings between the lower profits limit and the upper profits limit – and a new 1% rate was introduced on earnings above the upper profits limit. It was estimated that taken together these changes would raise around £7.9 billion in 2003/04. As tax rises go, this was popular and so there have been proposals to repeat the exercise.

“NICs are, in the words of Peter Bickley, technical manager at the Tax Faculty of the Institute of Chartered Accountants in England and Wales, “the Cinderella of taxes”. They are the unseen tax. They are a dream come true for chancellors of the exchequer. They are a tax that ordinary people, by and large, have not noticed.”

But is National Insurance a suitable vehicle to bear more of the increasing financial weight of the National Health Service?

It certainly has disadvantages. Firstly it does not bite on people above State Pension Age – ie the people who make most use of the NHS.

Secondly – it’s a tax on jobs. Employers pay an additional 13.8% on earnings above £153 a week. It does not bite on investment income, rents or dividends. So it does nothing to reduce the economic inequality which drives ill health. It has a number of perverse effects. NICs for employees are calculated on weekly earnings in each job. So people with two part time jobs pay less than those earning the same money in one job. People with fluctuating income can pay less than those with steady income. It’s a main driver for bogus self-employment schemes, because self employed people pay less, and their employers don’t have to make a contribution.

Thirdly, it’s regressive. Those earning above £805 a week only pay 2% NIC on their earnings above that figure

Taxation means that the richer man, because of his capacity to pay, pays more for the general purposes of the community. (Beveridge report para 273)

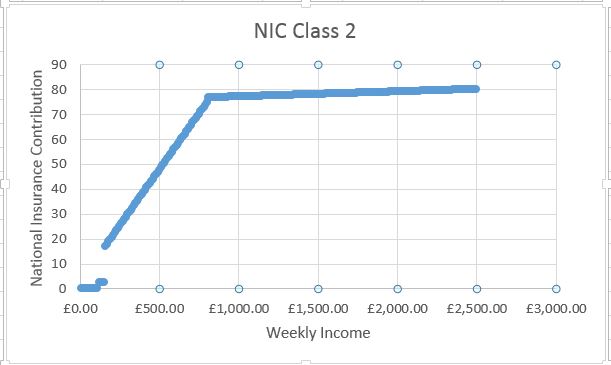

Self employed people are assessed on annual income. If they earn more than £41,865 per year they only have to pay 2% on their income above that level.

“National Insurance is not a true social insurance scheme; it is just another tax on earnings, and the current system invites politicians to play games with NICs without acknowledging that these are essentially part of the taxation of labour income.” Mirrlees Review 2011